The demand for single crystals at the investment end of the power station is growing;

The production line of the battery manufacturing end is continuously turned from polycrystalline to single crystal;

The mainstream enterprises of monocrystalline silicon wafers began to actively expand production;

Mainstream battery component manufacturers are beginning to plan the layout of upstream monocrystalline silicon wafers.

With the end of 2016, the 5GW single-crystal joint venture project of Tianhe, Tongwei and Longji shares, together with the launch of the former GCL and Jingke monocrystalline silicon wafer projects, and the downstream first-tier manufacturers to arrange the upstream monocrystalline silicon wafer production capacity. Officially announced the establishment of single crystal as a mainstream product trend.

And with the release of a large number of single crystal production capacity in the second half of 2017, the future industrial structure will undergo rapid changes.

At this historical turning point, we will review and forecast the competition of single polycrystalline route, and help you judge the future industry trends through objective figures and calculations.

The bottom gas of single crystal intake - the largest black horse information hidden in the semi-annual report is high-efficiency, but in the past it did have a high price of rickets.

At the SNEC exhibition in May 2016, Longji shares shouted the promise of following the 0.6 yuan spread of polysilicon, and basically implemented such a price strategy, and hoped to promote the increase of the single crystal market share. The picture below shows the price trend of single polysilicon wafers this year.

There are different opinions, but in fact the answer has already been given.

In the semi-annual report of 2016, the media of all major institutions have interpreted it, or missed the most critical information. The cost per wafer is lower than that of polycrystalline silicon.

Yes, most people may think that monocrystalline silicon wafers are costly, or at most consistent with polycrystalline at a cost per watt. In fact, the cost of each piece of monocrystalline silicon has been lower, which surprised the author.

Let's compare the semi-annual report data of the single polycrystalline faucet, GCL and Longji, and see how terrible the cost competitiveness of single crystal is.

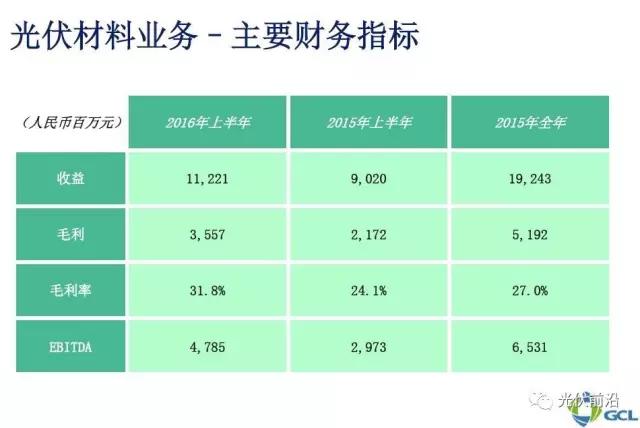

GCL's semi-annual report data

In the first half of 2016, the average price of wafers excluding tax was RMB 1.224/W.

Longji's semi-annual report data

(The following data section is selected from Xi'an Longji Silicon Materials Co., Ltd. 2016 Semi-annual Report)

In the first half of 2016, the output of monocrystalline silicon wafers was 667 million pieces.

Longji is actually 0.4 yuan lower than the cost of a single piece of GCL!

Don't worry, there are more amazing things.

Considering that the GCL silicon material is self-supplied, the Longji silicon material is externally produced, and the average selling price of the silicon material in the first half of the year is about 125 yuan. Longji's cost level under such premise of high-priced silicon materials is indeed quite powerful.

In other words, if the price of silicon material goes down, the cost advantage of Longji single crystal will be more obvious.

Assuming the price of silicon material goes down to 105 yuan, the cost of Longji single crystal will be reduced by about 0.3 yuan.

Moreover, the price of 105 yuan is not impossible. Considering the existing capacity of polysilicon material and the entry of new capacity in the future, the future is basically a situation of oversupply, and the price of silicon material will soon return to a reasonable price.

If the price of silicon material is stable at around 105 yuan, then the cost of single crystal silicon wafers of Longji is 0.7 yuan lower than that of GCL.

Yes, 0.7 yuan, this result may be hard to think of.

Seeing this, everything has become reasonable.

This is precisely the situation of overcapacity. Longji dares to invest nearly 10 billion yuan in succession and achieves the root cause of 22GW or more in 2018. It is also the reason why Central China dares to expand its production by more than 6 billion yuan and achieves more than 12 GW of production capacity in 2018. .

Jingke has chosen to self-invest and build 3GW monocrystalline silicon wafers due to the capacity and technology accumulation of monocrystalline silicon wafers. Jingao recently announced the purchase orders for single crystal furnaces;

Because there is no experience in the production of monocrystalline silicon wafers, Tianhe has not invested in the investment of the stoves. The accumulation of technology is also time-consuming. It is difficult to form a competitive force in the short term. Therefore, the financial investment is bound to the upstream production capacity, and the positioning of its downstream manufacturers is adhered to.

At present, the four major component manufacturers in China, only Artes has not yet acted, but it is said that it is already considering the layout of single crystal production capacity, whether it is on its own, or investment binding, I believe we will see similar actions soon.

to sum up

The bottom gas of single crystal is its solid cost competitiveness. Under the strength of at least 0.4 yuan per piece, the ability to execute its price-following strategy cannot be doubted.

Under such a strong cost strength, the trend of single crystal as a mainstream product was officially established.

The market structure in 2017 will show even greater changes.

1. Colorless, highly transparent water-soluble liquid, no health damage to construction workers, no damage to the living environment. 2. Good adhesion, excellent anti-fingerprint anti-dirty function. 3. Has a good antibacterial function. 4. Waterproof, oil proof, antifouling, antibacterial. 5. Anti-scratch, anti-friction, anti-handprint. 6. Easy to use, easy to clean, self-cleaning. 7. Colorless and transparent, improve the line of sight and improve the surface wear resistance of the product. 8. It is not decomposed by ultraviolet light and has weather resistance. It can be used indoors and outdoors. 9. Anti-friction, acid and alkali resistance, high temperature resistance

Nano Coating For Phone Touch Screen

Nano Coating Spray,Nano Coating Spray For Phones,Anti Fingerprint Coating For Phone,Nano Coating For Phone Touch Screen

Guangdong Giant Fluorine Energy Saving Technology Co.,Ltd , https://www.tuwtech.com